Can Your Valuation be too High?

How to mitigate the risks associated with raising capital at a high valuation

Yes, your valuation can be too high. In this article I will explain: (a) why that is the case; (b) when a valuation might be too high; (c) the risks associated with raising at an abnormally high valuation; and (d) critically, how to mitigate the risks associate with raising at a high-end valuation.

The issue is pertinent in today’s capital market mayhem. So many of us have drunk the kook-aid served during a once in a lifetime bull market that drove valuations unlike anything we have ever seen before. Fast forward to today and there’s blood in the streets. Flagship technology stocks are routinely down by 80% or more and word on the grapevine is that there is more pain to come.

Dozens of local technology companies are either battening down the hatches if they have capital to weather the storm or staring down the barrel of painful down rounds and layoffs.

Still, everyone is talking about the bygone ‘bull market’ as though they are disconnected from their own decisions within that market, not responsible for the 50x handshakes routinely being made between founder and investor. It’s time to ask, is my valuation too high?

Many investors won’t publicly say that irregularly high valuations are problematic. I believe there are two reasons for this: (1) investors need to justify valuations to their own investors. This is harder to do if you publicly promote that start-up valuations are too high; and (2) investors want to be seen by start-ups as bidders that will pay high prices in order to attract deal flow. But this is No BS VC and your valuation can be too high.

How can a market price be ‘too high’

For a start-up, a price that is too high is, in my opinion, one that is likely to present a material risk of a future down round. One could argue that the market determines a valuation but the start-up market is imperfect. There are limited participants and although a 100x multiple paid by an investor is by definition ‘the market’, there is little about it that represents a rational view on market value other than the definition itself. Whether your valuation is ‘market’ or not, if you can’t reasonably be expected to raise a following round at a higher price, it’s likely too high.

There are many things that impact your valuation in a market as flexible as start-up land. The supply demand equation oscillates regularly between bull and bear conditions and within this context, it is plain to see that if you:

raise capital at the highest price possible;

in a market that is red hot;

while your performance is exceptionally strong (particularly if it’s irregular or cyclical revenue);

from a specific category of investor that is inclined to ‘pay more’ for your type of business,

you are likely raising at the absolute peak of the market.

In some circumstances, pricing may be so high that it is disconnected from long term realistic and sustainable measures of value. Like all of us I have seen numerous businesses with flawed economics and little or no product raising many $millions at valuations of 10s of $millions.

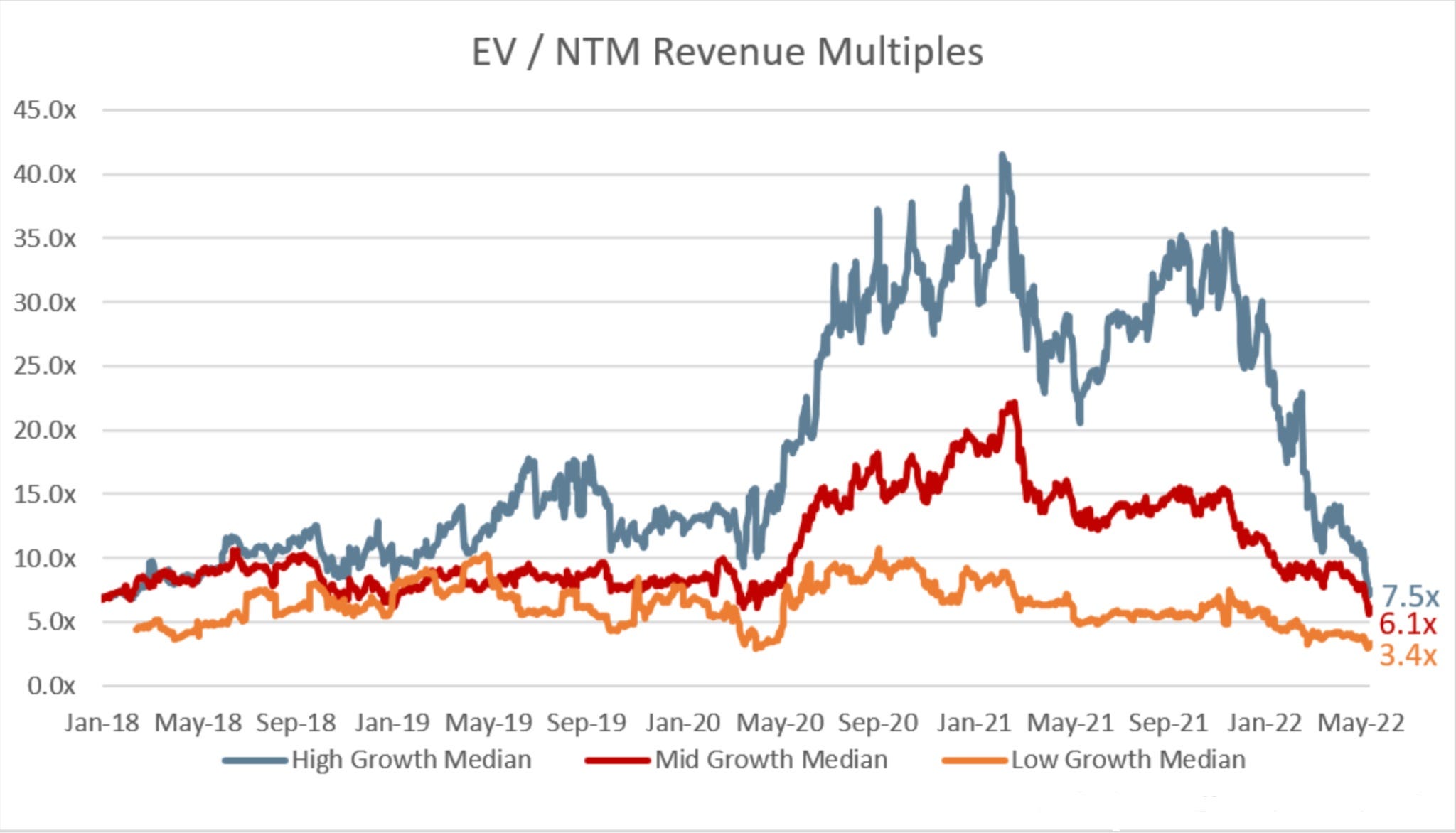

In an environment such as the current one where there remains a serious risk of multiple contraction going forward, then there remains a realistic scenario where even tripling a business in short order is unable to avoid a down round! Take a business at $10m ARR valued at $300m in their last funding round (commonplace in the last 12 months). If the revenue multiple contracts from 30x to 10x over the next twelve months (which is still 2x the current median multiple of listed tech companies) then the business needs to more than triple revenue just to sustain a flat valuation. Good luck.

If you are raising money at a price that is outside of mid-term market norms, you may be raising at a price that is too high to be sustained. If your valuation is not sustainable, your price is too high.

The risks

Start-ups that raise capital usually sign up to a plethora of legal rights and obligations. For example, investors will almost always have liquidation preferences, anti-dilution rights and reserved matters which give them the power to veto key decisions.

The risks here are obvious. To name a few: (a) investors may not support a capital raise at a price that is lower than their entry price, putting your business at risk if investors don’t support a new raise; (b) a down round triggers anti-dilution rights which can materially dilute shareholders; (c) down rounds are a negative market signal and bad for company morale, particularly if future valuations land below employee ESOP strike prices; (d) investors with liquidation preferences on large investments could take everything in the event of a down side liquidation event; (e) you could put yourself under enormous pressure from your investors as they pursue valuation uplifts from their last entry price… the list goes on. In truth, the issues associated with down rounds are somewhat self-evident. We all know down rounds are generally not a good thing albeit necessary at times.

How do you know if your valuation is too high?

This is an extremely hard question to answer as every business is different. My suggestion is to listen to the market and look at mid-term trends. If you have numerous offers at 10x revenue and someone bids 30x, it’s a pretty strong indicator that your pricing is outside of market norms.

Most investors and community participants will give you valuation feedback. Listen to this. It’s no secret that investors have an interest in pricing opportunities at lower multiples but they are also generally decent and honest people. I have seen and been part of many investment rounds where the investors actually pushed pricing up to limit founder dilution in a way that benefits the company and allows it to raise the money it needs to succeed.

Listen to the market.

Mitigating the risk

Let’s be honest, there are a LOT of good reasons to raise capital at the highest price you can. I am not here to suggest this is a bad idea, it often isn’t. I am here to try and help you navigate the process.

Ironically, for the reasons above, the higher your valuation the greater the risk the round presents to you. If your valuation is ‘high’, you should be sensitive to the legal mechanisms which impact your future capital planning as the risk of a down round is high.

Founders have to tread a fine line between minimising dilution and partnering with the investors they want to work with. If your valuation is ‘abnormally high’, these suggestions might help you mitigate the inherent risks:

1. Raise enough money

This is perhaps the most important point to consider. If your pricing is irrationally high, there is always a good chance your next round will not be and so you need enough time and money to build your business to the point that you can put forward a rational case for being priced at or above the current valuation. Make sure you raise enough money to grow into your valuation. Admittedly, this is always the case for all raises, but it is even more important to consider if the valuation of the current round is high, you will need more time and more money to grow into this valuation.

2. Anti-dilution alternatives

Anti-dilution rights in essence give additional shares to investors that hold these rights in circumstances in which your valuation drops.

There are broadly two mechanisms use, full ratchet and weighted average anti-dilution. The former is now seldom used and far more aggressive. Never agree to full ratchet anti-dilution.

Beyond this, one newer solution that has been developed for founders to offset the effect of unfavourable anti-dilution terms is a “pay to play” clause. Given investors are protected from dilution, they may not be incentivised to participate in a down round, particularly if performance is poor. I have seen this a lot. A pay to play clause may require investors participate in a future round of financing in order to receive anti-dilution protection. I rarely see this used and so your investors may not be expecting it but if your valuation is high end, it may be worth the effort of negotiating this.

3. Reserved matters

Investors will often require you to seek their approval before raising capital. If your valuation is high and a down round is more likely, it is also more likely that your investor may oppose future capital raising. An investor facing a write down can be a difficult person. You should be more sensitive to this right if your valuation is ‘high’.

4. Diversify your investor base

Often, at an early stage, less is more when it comes to the number of investors. You’re a small business and you need to be nimble and efficient and more investors generally means more communication, more lawyers and more perspectives (which does have benefits too). When raising a large amount of money at a price that is generally outside of market norms, my view is that the risks associated with future down rounds outweighs the need for simplicity. More investors means less capital dependency. If the market or your performance or anything else doesn’t go to plan, it will always be easier to raise money from investors that are already in the tent and having 5 investors to ask for money instead of one can may make life easier.

5. Understand your investors mandate and capital base

Given down rounds are usually sponsored by existing investors, it is important to understand whether your investors have capital and a mandate to support future rounds. Where your valuation is ‘normal’, you are much more likely to be able to access capital at a higher price from third parties. Where it is not normal, you want to ensure your ‘not normal’ sponsors are going to be there to sponsor a few more ‘not normal’ rounds.

I have, for example, seen corporate investors that don’t have a mandate for follow-on investing cut large cheques at very high prices after which the company is sent into the venture community to find future capital. The venture community is often more price conscious than large strategic investors and so it is easy to see how this can be problematic.

6. Plan ahead

Start-ups often do a good job of business planning but sometimes a poor job of capital planning. Capital planning is similar but different and even more important when you raise large amounts of money at high prices.

If your next round does follows an abnormally high valuation, you should effectively understand what you will need to do in order to achieve a valuation above the price of the last round. This may involve international expansion, growth, product or any other metric needed to support a certain price. Talk to your investors and understand what you need to achieve here. Once you understand what’s needed, you should ensure you have the time and money you need to get there. If you think you might not, you should be aware of this way ahead of time and discuss it with your board so that you can plan for it.

Down rounds are most common when companies run out of money unexpectedly. Effectively capital planning around the initiatives required and the corresponding timeframes and cash runway needed can mitigate this risk.

7. Find a capital partner you trust

This is, above all, the number one thing you can do to mitigate your risk. Partner with someone that you trust. There are numerous actors in the investor community that will pay almost any price in some circumstances, often because they aren’t entirely in tune with market norms. Unfortunately, those most willing to ‘overpay’ are often those with less start-up investing experience and/or irrational and in addition to this are by definition well funded which means they can afford the cost of a lawyer if they aren’t happy with you. We have all heard the sometimes unfairly derogatory term ‘dumb money’ before. It’s a balancing act between raising at a ‘good’ valuation and finding a partner that you like a trust. If you can, get both. It would be a high-risk endeavour to raise money from a party that you don’t entirely trust on the basis that their valuation is above and beyond the general market landing.

Our approach to this is to connect prospective investees with the other founders we work with so that you can get hear about us from someone on the ground. Do your diligence on your investors just like they do your diligence on you.

Raising money at the highest price possible is often the right answer, but not always. If you’re unsure what to do and you’re likely to take money from a person that is paying a lot more than the rest of the market, hopefully these tips help you limit the associated risks.

If you’ve enjoyed reading this, please share it! If not, please tell me why?

Happy investing.

Dan